About me: I am a full-time emergency medicine doctor a few years out of residency (finished in 2020, currently 37 years old). I currently work in various emergency departments as a 1099 contractor and have a few telemedicine side gigs. I am married to my beautiful wife, Mrs. AMJ and have one child. I created this blog to track my financial journey. My goal is to maintain a balanced approach to my finances between slowly paying down my low interest debt, investing aggressively, but also enjoying life along the way (IE: Somewhere between frugal and YOLO). Thank you for following along.

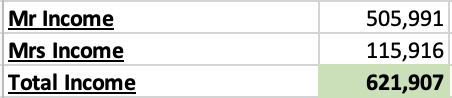

2025 Total Income*

*This represents our income from working our regular jobs.

2025 Other Income:

This year was a messy one with a lot of good times but a lot of hard times. I paid off my remaining student loans ( $100k this year, approximately $301k in total), we dramatically grew our stock market portfolio by almost $1 mil. I also lost a close family member and this being a financially focused blog, I received a moderate inheritance (around $300k). I started working for another nearby ER group part time and also grew my telemedicine work, this allowed me to drop to part time/PRN at my main job which I had been working fulltime for the last two years. For various reasons, I had become unhappy/annoyed at the main job and having other gigs/income while making huge strides financially allowed me to step back a bit. My wife also continues to work a part time w2 job which gives us great benefits and allows me the flexibility to work as a 1099 contractor. Financially, we are in a much better place than we were just a year ago.

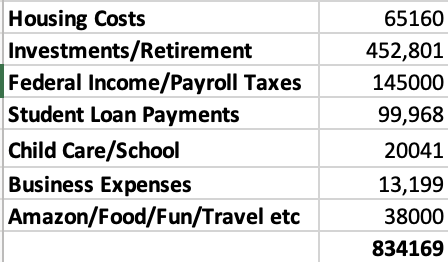

Excluding the Inherited IRA, I had $834k in cash to work with. Let’s run through where all this month went:

Lets’ go through each line item:

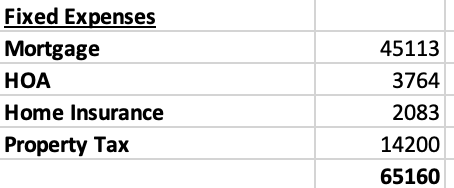

Housing:

Despite living in Florida, our insurance is reasonable, this does not include flood insurance (we do not carry). We thankfully did not have any major expenses or repairs this year (We custom build a home in 2022-2023 thus everything is still new).

I finally paid off my student loans. I started the year with 100k left and two years left of a 5 year payment plan at 1.1%. I invested about 10k in PLTR stock over the past few years and the stock skyrocketed. Once that stock became almost equivalent to my remaining student loans and said screw it and I sold all my PLTR and wiped out my student loans for good. Some regret as PLTR continued to skyrocket and I could have sold with an additional $50k gain later this year, but the payments were bigger than our mortgage so it really cut our living expenses in half by not having that monthly payment.

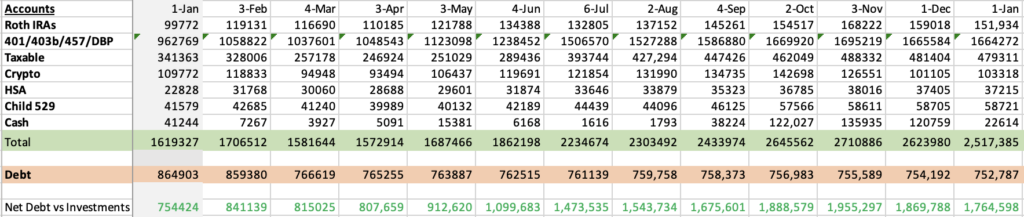

Above is a breakdown of our investments. I work as a 1099 contractor and have set up a solo 401k plus a DB Plan. This allows me to invest much more pretax than I otherwise would be eligible for. I had not yet funded any of my 2024 plan so I funded that amount and then funded the rest for 2025 before the end of the year. My wife has a standard 401k with small match and a 457 plan we max. I have a goal to contribute 10k each year for my sons college fund (goal is 18 years at 10k = 180k contribution) and I contributed 20k this year. We do backdoor Roth IRAs and max our family plan HSA as well. Anything extra, we put in our taxable account. Some of this taxable money was related to inheritance received, all total I contributed $452k.

Our tax payment bill was much bigger than I wanted but part of this was an additional 20k or so required for the PLTR sale (LTCG 15% plus NIIT tax).

Our investment gains for the year are $388,431 when you include PLTR stock sale profits.

Child care came in around 20k as our son goes to part time school (daycare really) and we have a nanny for two days a week when we are both working. We are discussing full time school next year and this will slightly drop cost for us as home nanny is much more expensive.

Business expenses were fairly standard for the year, CPA, taxes, LLC, licensing, credentialling all adds up.

The rest covers really food/living expenses etc. We took only one “expensive” vacation that cost about 6k, otherwise we visiting family or traveled locally thus our day-to-day expenses at home are fairly low.

Investments:

Investment Account Breakdown

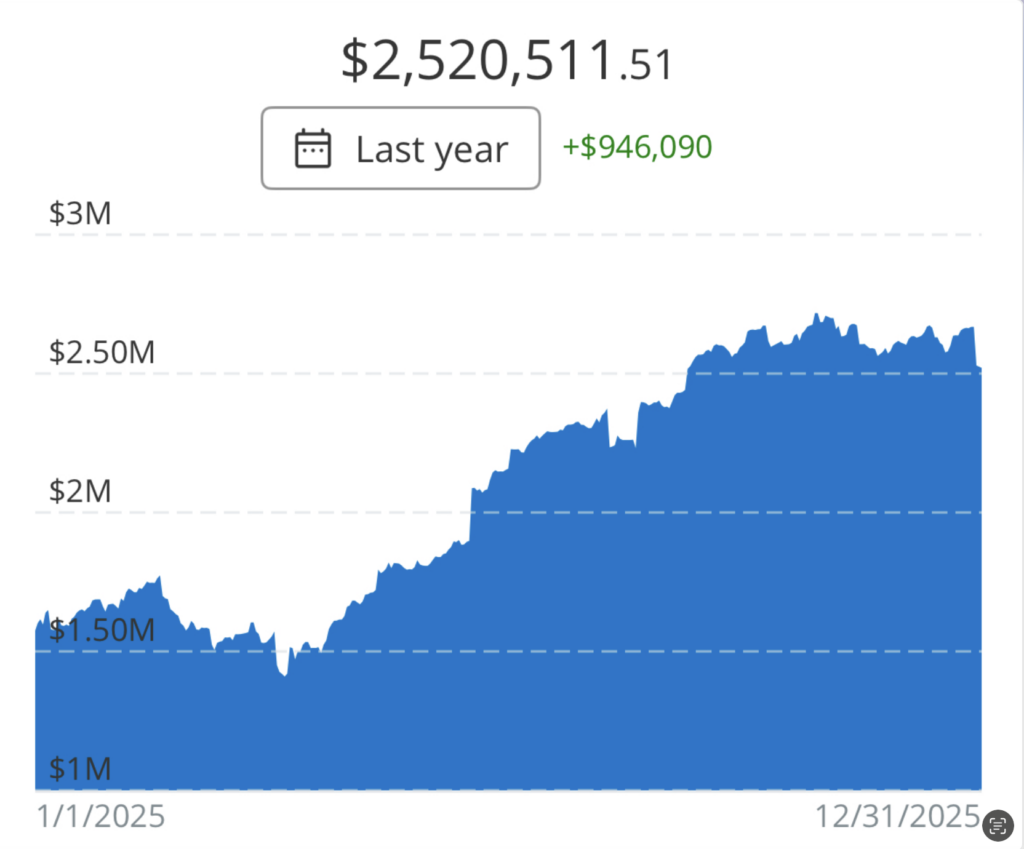

My mind is blown at how much progress we have made since just 2-3 years ago. Compound interest and snowballing really starts to take effect once you cross $1 mil.

Lets look back at my financial goals for 2025

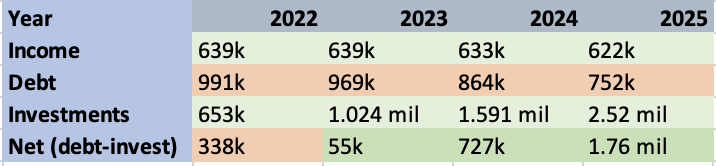

- Hit $2 Million in investments. Currently at approximately $1.6 mil, I plan to put in at least 200k, that requires a market return of about 10% to get me to $2 mil.

- Goal hit and we crossed $2.5 mil

- Pay off remaining student loans. I start the year with ~$95k left in student loans refinanced to 1.1%. I know mathematically it makes zero sense, but I only have two years left on them regardless. I plan to fully fund my retirement accounts in the first quarter of 2025 and then have them gone by midway through the year.

- Goal hit in February as I sold off my PLTR stock and made one final lump sum payment

- Work less? I said that last year, didn’t happen.

- Finally, can say I am doing this

Looking forward to financial goals for 2026.

- Hit $3 million in investments: Currently just over $2.5 and I hope to contribute at least 200k this upcoming year. Will need a little bit of growth in the market but it seems doable.

- ?Pay down mortgage and recast. Our mortgage has a rate of 3.75%. My wife and I have entertained the idea of paying it down a bit and recasting to drop the payment in case something ever happens to one of us. Our current payment is around $4k/month.

- Obtain umbrella insurance – Expensive in my home state (almost 1k for the year), I haven’t been able to bring myself to buy it yet, but I know I need to. This year is the year!

I cut back from full time emergency medicine work starting in October and I feel so much better, happy and healthier. I am now able to exercise consistently each week. I get to spend a lot of time with my son and my relationship with my wife has also much improved with the decreased clinical load. While this blog remains financial in nature, ultimately what matters in life is your health and relationships with the people that truly love you. Growing and securing my financial future has dramatically changed my life for the better.

Thanks for following!

-AMJ