Early career Emergency Medicine physician trying to navigate the financial world

- June 2026 Update

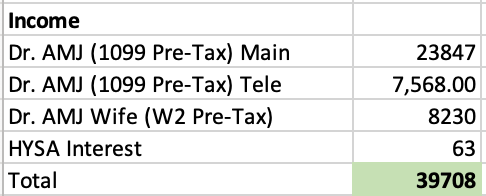

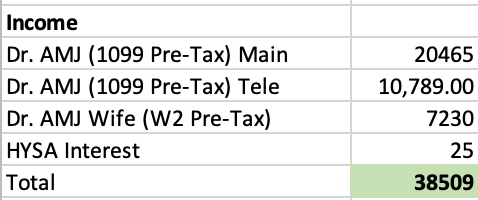

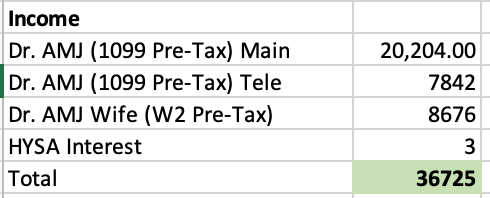

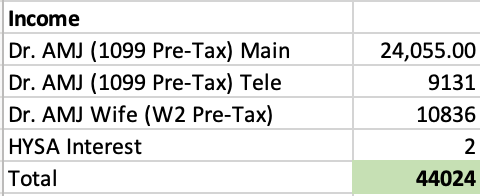

June Total Income:

Another busy month for us, I ended up working 13 clinical shifts this month as the ER groups I work for are super short staffed and begging for work. My director called me and offered increased pay to do so. That meant I did very little telemedicine this month as we had a vacation and a few fun short trips planned on days off. L

Life has really become a lot more fun and enjoyable being a “part time” doc, particularly no longer working night shifts has made me much happier and likely healthier too. It is somewhat hard to accept lower monthly income (compared to what I can and was previously making), but I remember how much we have done on the investing side and it’s worth it for the long term.

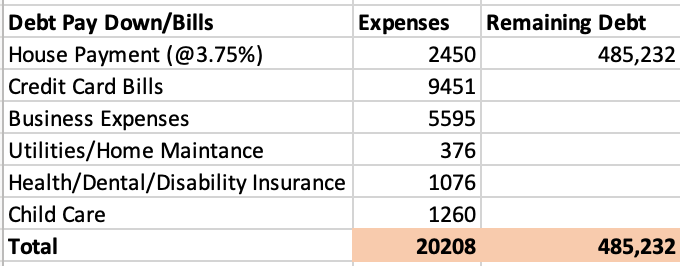

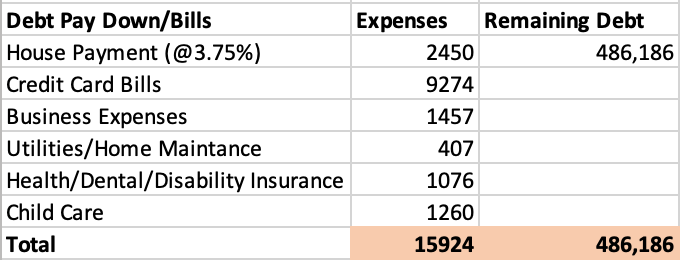

Expenses

I continue to be surprised at how much our expenses have increased over the last year or so. We have had a lot of maintenance items come up on our home and boat this year greatly increasing our usual expenses and there is likely more to come. We have also started to open up a bit on our spending with vacations, weekend trips, etc. The other big bill this month was for my CPA/payroll/tax stuff.

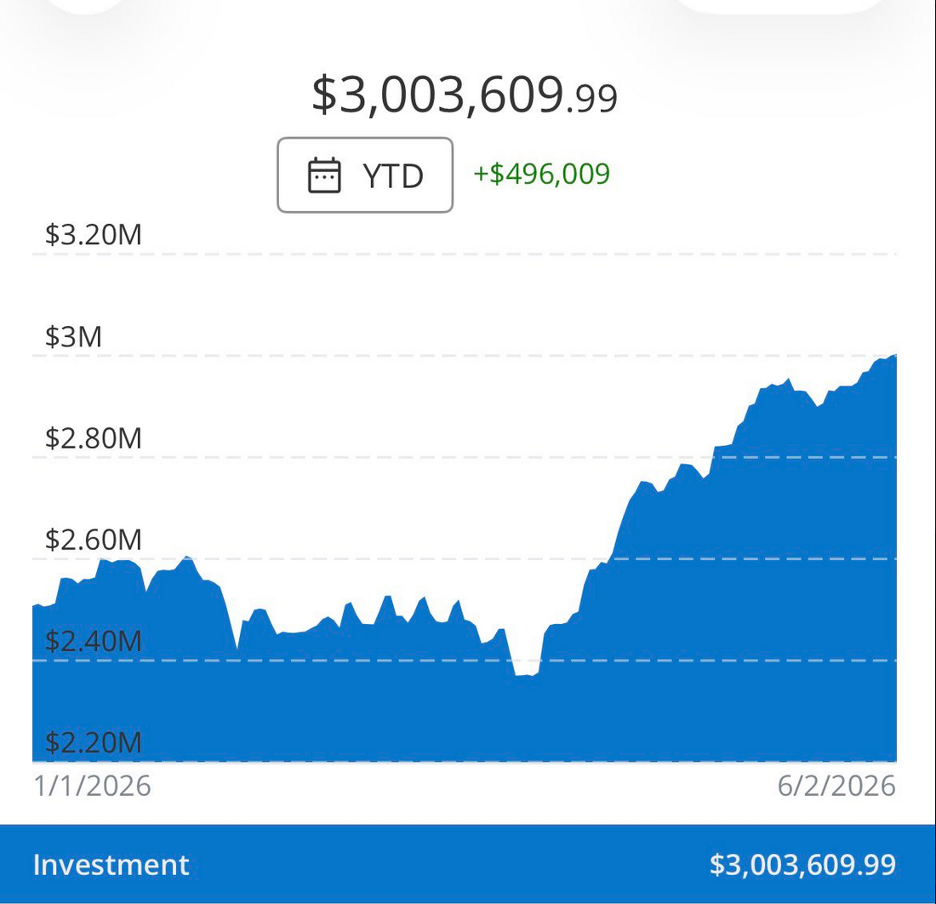

Investments

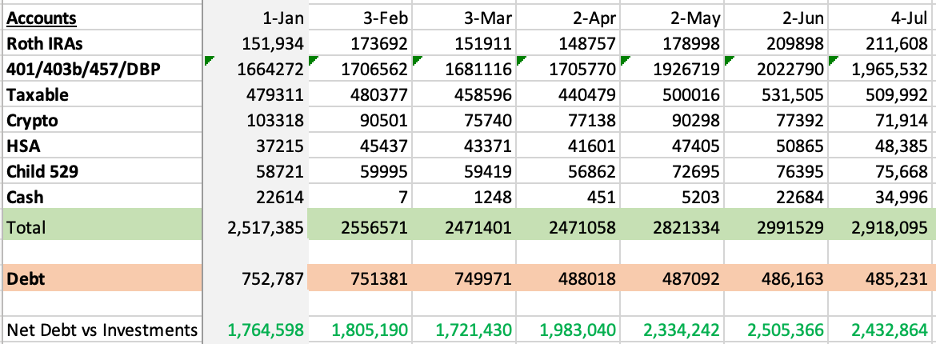

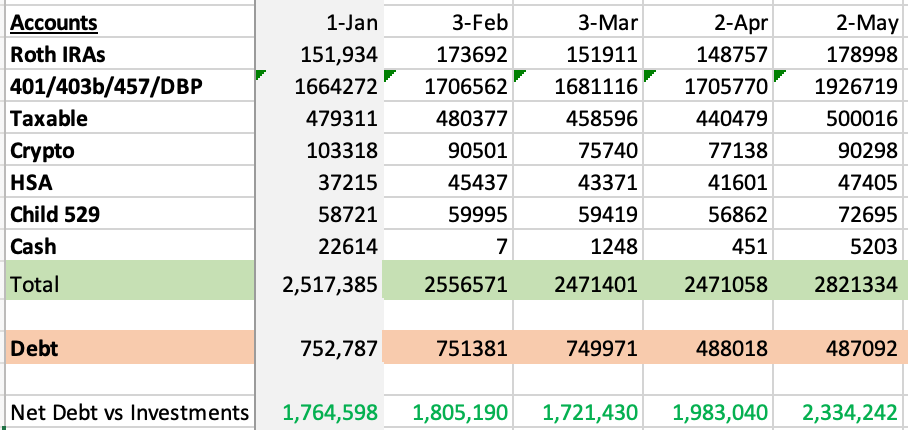

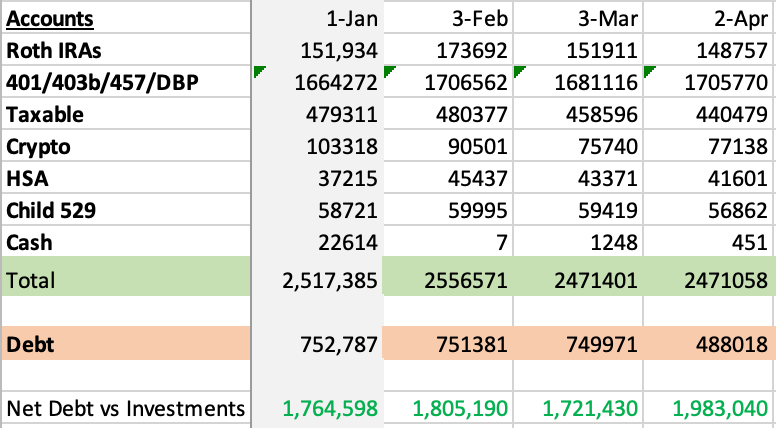

While we hit $3 mil briefly in early June, the market and crypto dumped pretty hard thereafter and we came back down to reality.

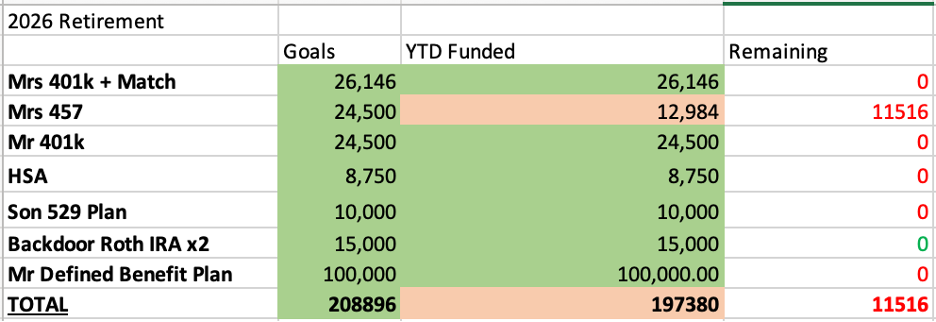

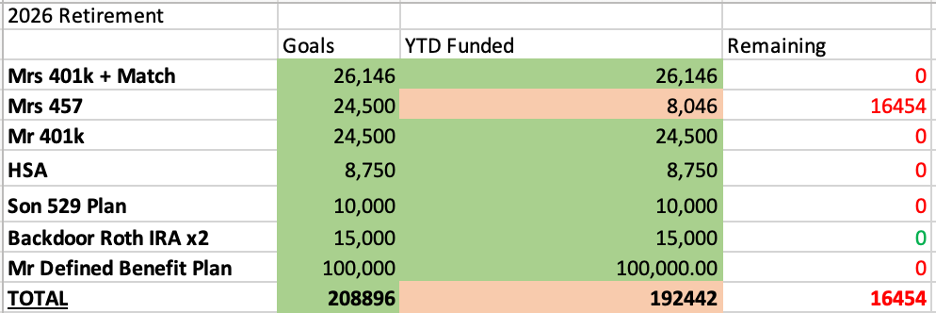

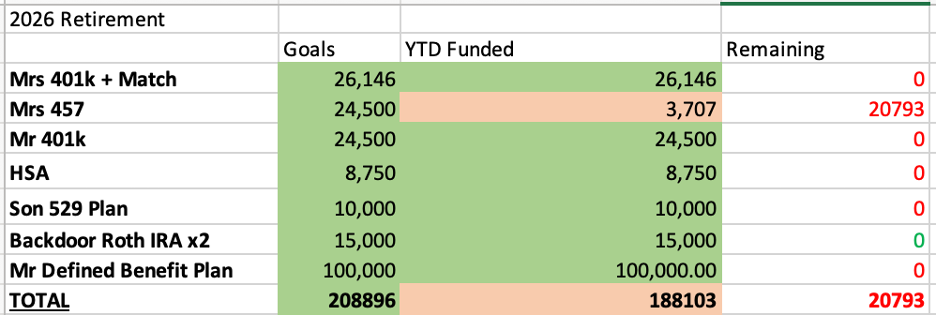

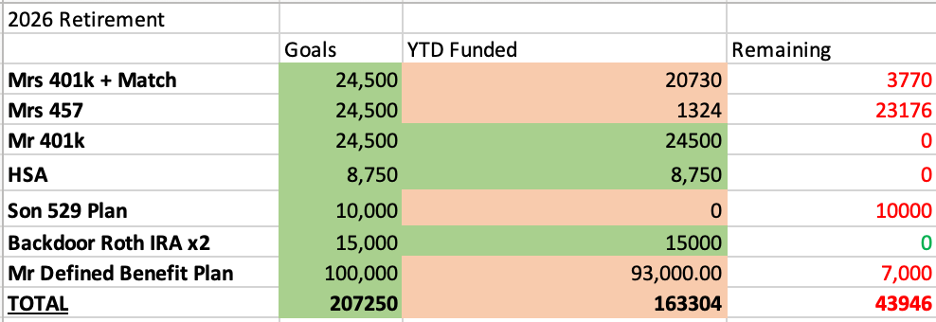

No major changes with our retirement contributions, my wife continues to contribute to her 457, about 11k left so should be maxed in about 2 more months. I continue to save up for my end of year S corp tax bill.

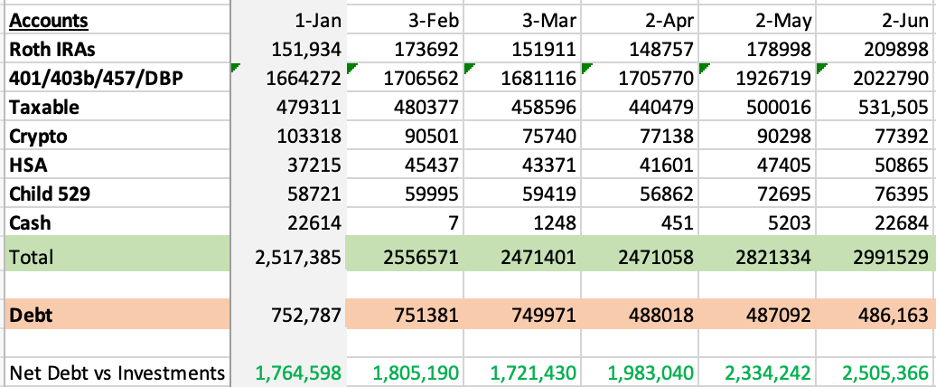

Investment Accounts:

Slight drop for the month but still trending up and to the right for the year.

My Financial Goals for 2026

- Hit $3 million in investments: We did this, June 1st!!!!!

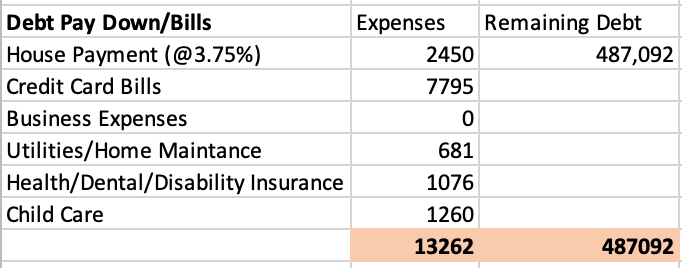

- Pay down mortgage and recast – DONE – 260k extra payment (family gift) and mortgage recast done, payment changed from $3,759 $2,450

- Obtain umbrella insurance – DONE! We finally obtained a $1 mil policy.

-AMJ

- May 2026 Update

May Total Income:

Another month with our income on the lower side. I’ve honestly probably never been happier in the past few months despite a decent pull back in our income. Having moved to half time clinical shifts in the emergency department allows me to get out of night shifts (which I hate). Most recently, I got offered an extra $1000 cash to work a night shift (thus about $4,000 total) for a single night shift and happily turned it down.

I’ve got a spend a ton of time with my wife and son, doing lots of weekend trips and adventures together which has been a lot of fun. With the stock market ripping the last two months, our net worth continues to climb despite a drop in income.

Expenses

Last month, we went on an all-inclusive Caribbean vacation so we had a lot of extra expenses related to that. The trip was amazing and probably cost about $15,000 in total. This is the big reason our credit card bill are so large and total expenses almost $16k for the month. I had some licensing fees I had to take care under business expenses.

Investments

$3 million!!!! Crazy how much our accounts have grown over the past three years. The market continued to go nuts in May and we finally breached $3 million. Crypto/bitcoin has taken a large dip from last year.

My wife continues to work on her 457 contributions. Otherwise, I am now saving up cash for end of year tax payments and other big expenses (S corp taxes, property taxes, school tuition, etc)

Investment Accounts:

A net positive change of $171k for the month. Compound interest has taken over.

My Financial Goals for 2026

- Hit $3 million in investments: We did this, June 1st!!!!!

- Pay down mortgage and recast – DONE – 260k extra payment (family gift) and mortgage recast done, payment changed from $3,759 $2,450

- Obtain umbrella insurance – DONE! We finally obtained a $1 mil policy.

-AMJ

- April 2026 Update

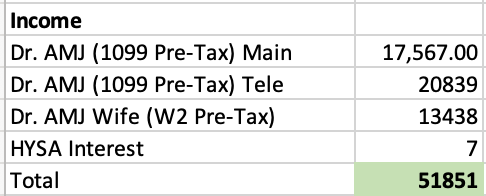

April Total Income:

Definitely a lower income month for us. We had family visiting the beginning of the month and then took a vacation the last week of the month so really only had two weeks of full work. Thankfully the stock market rebounded significantly this month.

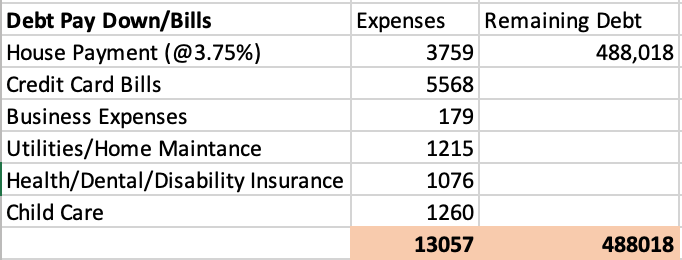

Expenses

This is our first month with our newly re-casted mortgage payment, now $2450 (previously $3759). I continue to be surprised how high our monthly credit card bills have become, it seems like every month we have an unexpected issue with the house, car, maintenance, etc. We purchased some Ikea closets and then had an unexpected plumbing issue this month resulting in some extra expenses.

Investments

The market took a wild upward swing in April. Our investments dipped below 2.4 mil and by the end of the month, grew to 2.8 mil. Totally wild swing of 400k in just one month. Just goes to show you how important it is to just stay invested for the long term.

I have now hit my initial investing goals for the year, my wife just has to max out her 457 which she should be able to do within the next 2-3 months. I am now planning to save up a cash cushion to pay for end of year taxes. Once I have enough saved (likely around 100k), I will contribute some more to our taxable account.

Investment Accounts:

Again, we experienced a wild swing up in the stock market this month. Our delta on debt vs investments was 351k. Hope we continue to see some market returns for the year!

My Financial Goals for 2026

- Hit $3 million in investments: We are currently at the $2.8 mil range, contributions continue to go in every month, need some growth in the market to achieve this goal.

- Pay down mortgage and recast – DONE – 260k extra payment (family gift) and mortgage recast done, payment changed from $3,759–> $2,450

- Obtain umbrella insurance – DONE! We finally obtained a $1 mil policy.

-AMJ

- March 2026 Update

March Total Income:

I ended up skipping last month’s update, had a lot going on. I honestly was debating whether or not to continue on with this blog. We reached a lot of milestones and now seem to get more trolls as we move along our financial journey. I did get some encouragement online about continuing to post so I’ve decided to continue on for now.

No major changes to our income this month, I continue to work part time emergency medicine with 8-10 clinical shifts a month and then supplement my income with telemedicine work. Thus far, I am very happy with the change and feel it is much more sustainable in the long run than full time clinical emergency medicine. My wife continues to work part time in the hospital as well.

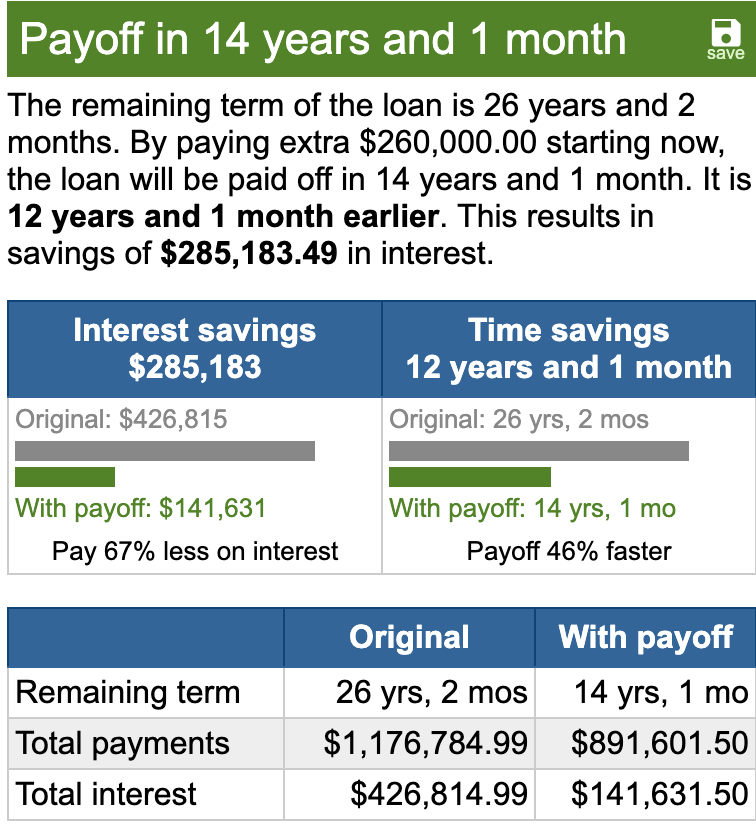

Now, on to the big news for this month, we received a gift from my wife’s parents of $260,000. We had a lot of discussion on what to do with this gift, ultimately, we decide to pay down our 3.75% mortgage (mortgage was $750k $490k). While I fully acknowledge we could have put that money in the stock market and likely done much better, we didn’t. A few reasons

- The money was a gift from my wife’s parents after they sold their primary home and downsized to a condo. We received a portion of that money from the house sale. The house was my wife’s childhood home. My wife’s parents both came to America as immigrants with nothing. They worked hard and achieved in American dream. In fact, her father (who worked in construction) spent 2 years building the home himself. We felt in someways, it was a tribute to them to transfer the money into our house.

- We have built a nice nest egg for our late 30s (+/- $2.5mil invested in the stock market) and felt it was reasonable to take some risk of the table with a large paydown of our debt.

- Our state has homestead protection, thus no one can come after our house/home equity so there is some asset protection.

- Recast – We applied to recast our mortgage. The payment will drop from $3800 ~$2400 (do not have final numbers yet). In case one of us loses our job, it lowers our monthly fixed costs. Of course, we will always have the option to pay more if we desire.

- We saved $285k in interest over the course of the loan (see numbers below):

Would you have done the same?

Next, I also received a large tax refund of just over $40,000. I did have a discussion with my CPA about it, overestimated capital gain taxes (had some tax loss harvesting from the previous year) resulting in a large refund. I immediately deployed this month into my defined benefit plan as I continue to aggressively fund all of our retirement accounts for the year even as we’ve had a big market pullback.

Expenses

I continue to be surprised with how expensive life seems to have gotten within the past few years. We continue to have (thankfully) minor maintenance issues with our cars, house, boat, etc and always seem to have extra unexpected bills each month. Our monthly credit card expenses are now routinely over $5k. Regardless, we haven’t had any major expenses this year so we are still counting our blessings.

Investments

Ouch, it has been a tough start to the year. Empower shows us down about 10% for the year although we got a little boost back up at the end of the month. Regardless, we continue to invest every extra dollar we can.

$163k we have invested into various tax protected accounts this year. Again, some of this money was extra cash we had leftover from the year prior and I also put my $40k tax refund into my defined benefit plan giving us a nice boost to get that maxed for the year. Next month, I am planning to max the DB plan ($7k more) and then also add $10k to my son’s 529 plan. After that, I will start saving up our funds for taxes (usually try to have around $100k cash by the end of the year as I file as an S-corp with a single payroll in December allowing me to pay my tax bill at the end of year).

Investment Accounts:

Ouch, hard to see our investments down so much, but we continue along and know it will grow in the long term.

My Financial Goals for 2026

- Hit $3 million in investments: We are currently at the $2.5 mil range, contributions continue to go in every month, need some growth in the market to achieve this goal.

- ?Pay down mortgage and recast – In process

- Obtain umbrella insurance – Done! We finally obtained a $1 mil policy.

-AMJ

- January 2026 Update

January Total Income:

We are off to a good start for 2026, my wife got three paychecks this month so her income ended up being a little higher than usual. I continue to work several “PRN” or part-time jobs via telemedicine and various local ER gigs. So far, I am much happier with this hybrid schedule.

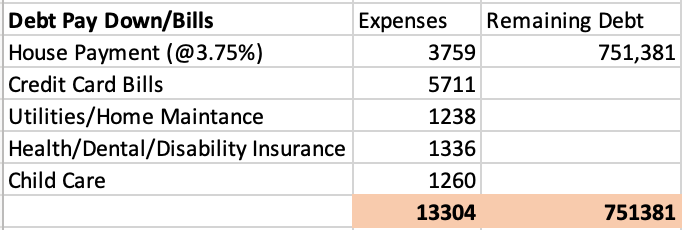

Expenses

We had several maintenance items come up this month, often saying to myself, “the joys of homeownership”. pluming issues, dryer vent issue, landscaping upgrades, thankfully nothing major but enough to up our usual expenses for the month.

Investments

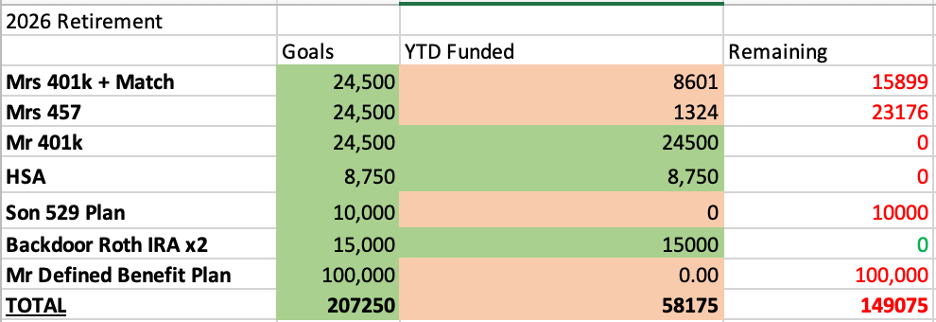

We continue to aggressively invest every dollar we can. I emptied out our HYSA to deploy into our retirement accounts:

HSA, my 401k, Backdoor Roth IRA x2 all maxed this month. My next goal will be max out my DB plan for the year which will take at least 4-5 months as I have a goal of 100k in that account for the year (I get my final numbers at the end of the year but prefund most of it).

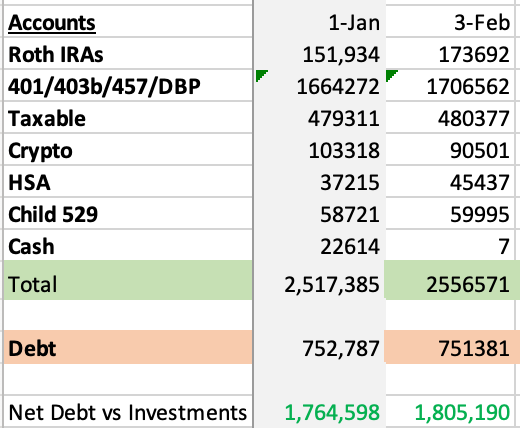

Investment Accounts:

A net gain of $41k for the month.

My Financial Goals for 2026

- Hit $3 million in investments: We are currently at the $2.5 mil range, contributions continue to go in every month, need some growth in the market to achieve this goal.

- ?Pay down mortgage and recast. Our mortgage has a rate of 3.75%. My wife and I have entertained the idea of paying it down a bit and recasting to drop the payment in case something ever happens to one of us. Our current payment is around $4k/month.

- Obtain umbrella insurance – Expensive in my home state (almost 1k for the year), I haven’t been able to bring myself to buy it yet, but I know I need to. This year is the year!

-AMJ